The fintech industry in 2025-2026 continues to evolve rapidly, with many companies pursuing their own bank charters for greater control, lower funding costs, and reduced dependency on intermediaries. However, sponsor banks—traditional institutions that provide regulatory access via Banking-as-a-Service (BaaS) models—remain indispensable. Even as fintechs scale and seek independence, sponsor partnerships offer resilience, specialized capabilities, and risk mitigation that self-chartering often cannot fully replace.

Why Sponsor Banks Remain Essential for Fintechs (even as they pursue charters)

Sponsor banks provide foundational infrastructure that allows fintechs to launch products quickly without the multi-year, multi-million-dollar burden of chartering. Even charter-holding fintechs like Nubank or emerging applicants often retain sponsor relationships for specific products, geographic reach, or risk diversification. Charters grant independence in lending and deposits but introduce heavy overhead—strict capital requirements, ongoing supervision, and operational shifts from tech agility to banking compliance. Sponsor models enable focus on innovation and customer acquisition while leveraging the bank's established rails, FDIC insurance credibility, and compliance expertise. In 2026, as regulatory windows for charters may narrow, sponsors offer a proven, lower-risk path for many fintechs, especially those not balance-sheet centric.

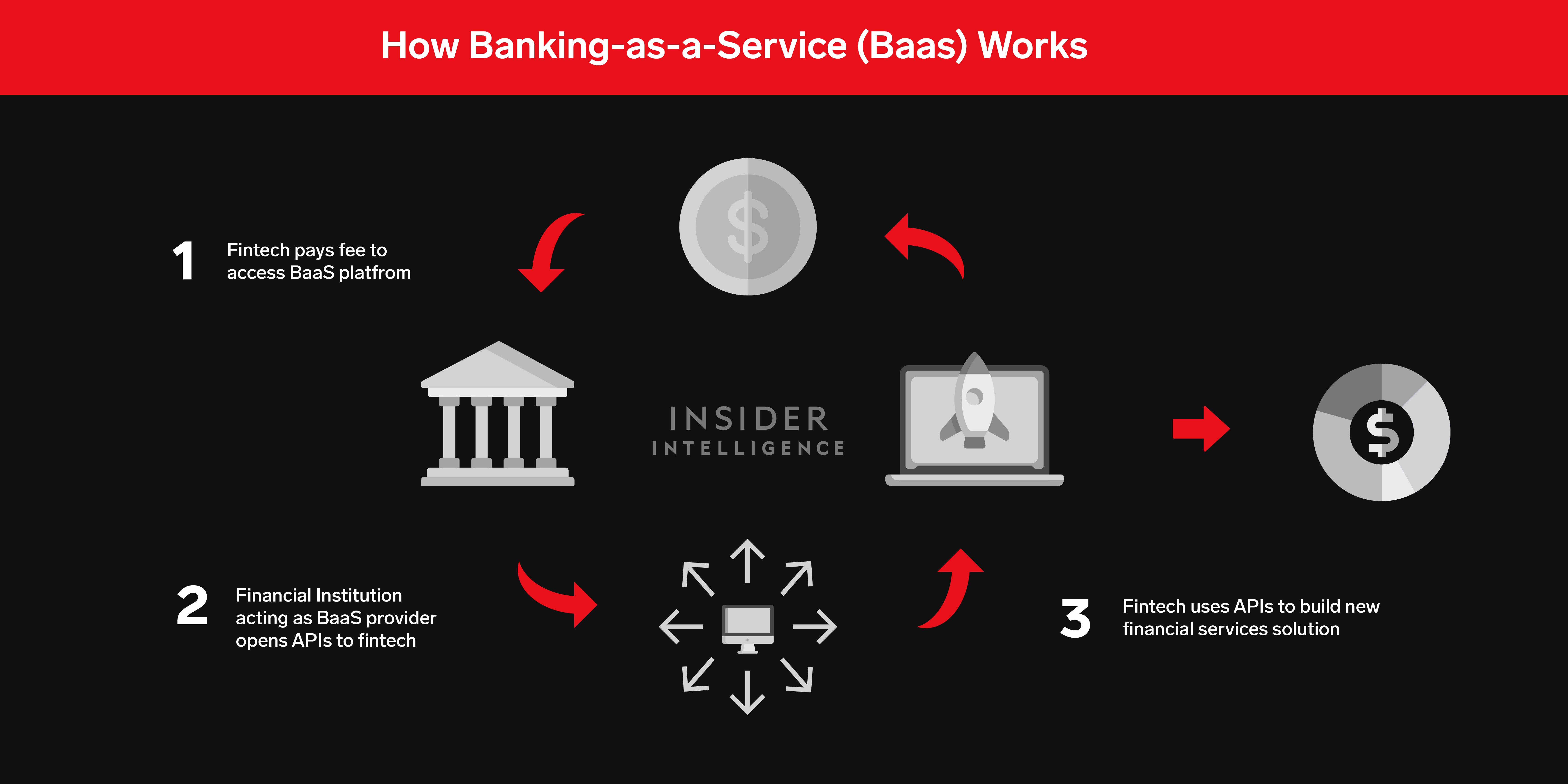

This diagram illustrates how BaaS works: fintechs access sponsor bank infrastructure via APIs to deliver services efficiently.

Banking-as-a-Service (BaaS) Scrutiny and Compliance Burden

BaaS has faced intensified oversight since 2023-2024 enforcement actions, with regulators targeting third-party risk management, AML/KYC controls, and consumer protection in sponsor-fintech setups. Sponsor banks now demand rigorous fintech compliance—real-time monitoring, independent audits, and granular data access—to avoid consent orders. This burden has matured the ecosystem: sponsors are more selective, prioritizing partners with strong controls. For fintechs, this means higher standards but also more stable partnerships. The scrutiny has cooled slightly under recent administrations, yet it reinforces sponsors' value in handling complex regulatory navigation that chartered fintechs still face in full.

Here’s a visual of layered compliance risks in BaaS models, showing sponsor banks overseeing multiple intermediaries for fraud, KYC, and AML.

Fintechs Racing for Bank Charters (vs. sticking with sponsor models)

The rush for charters stems from scale: at critical mass, interest income dominates revenue (e.g., 25-50% for firms like Revolut or Robinhood), making sponsor fees and counterparty risks costly. Charters unlock cheaper deposit funding, national lending without state usury limits, and direct Fed access. However, many fintechs opt for hybrid approaches—chartering for core activities while retaining sponsors for debit cards (to avoid Durbin caps) or specialized products. Sponsorship remains ideal for non-lending-focused fintechs, offering faster entry, less overhead, and favorable treatment in supportive regulatory climates. The race is real, but sponsorship endures for agility and risk mitigation.

Hidden Costs and Valuation Risks of Fintech Banking Licenses

Obtaining a charter involves substantial hidden costs: paid-in capital requirements, building compliance infrastructure from scratch, hiring specialized personnel, and diverting focus from growth. De novo formation takes years with uncertain success, while acquisitions carry integration risks. Valuation impacts are significant—fintechs trade at high multiples (8x+ book value), but banks often at 1-2x, potentially compressing multiples if the model shifts balance-sheet heavy. Sponsors eliminate these by offloading overhead, allowing fintechs to maintain tech-like valuations while accessing banking benefits indirectly.

Why Fintechs Need More Than One Sponsor Bank (diversification, continuity, leverage)

Single-sponsor dependency exposes fintechs to partner-specific risks—regulatory actions, exits, or operational failures (e.g., past collapses). Multiple sponsors ensure business continuity (no service disruptions), broader capabilities (different banks excel in payments, lending, or international wires), and negotiation leverage for better terms. Diversification mitigates concentration risk, enhances compliance flexibility, and supports product expansion. Mature fintechs increasingly adopt this strategy for scalability and resilience in volatile environments.

This infographic highlights third- and fourth-party relationships in sponsor models, emphasizing diversification needs.

Embedded Finance and the Future of Bank-Fintech Partnerships

Embedded finance—integrating banking into non-financial platforms—drives the next wave, with projections exceeding $138 billion by 2026. Sponsor banks power this by providing APIs for seamless deposits, payments, and credit in apps like ride-sharing or accounting software. Partnerships evolve from middleware to direct, symbiotic models: banks gain deposits and reach, fintechs/merchants gain revenue streams. The future favors mature, compliant collaborations over growth-at-all-costs, with sponsors enabling embedded scale while managing risks.

A clear flow showing how embedded finance connects customers, brands, BaaS platforms, and sponsor banks.

Heightened Regulatory Oversight of BaaS Models

Post-2022 enforcement (e.g., FDIC actions on BSA/AML and third-party risks) has heightened scrutiny, with sponsors required to exert demonstrable control. Oversight focuses on governance, fraud prevention, and reconciliation. While eased in some areas recently, regulators demand robust frameworks—independent testing, risk assessments, and data visibility. This professionalizes BaaS, making strong sponsor relationships a compliance asset rather than a liability.

Sponsor Bank Competition in the Fintech Era

Competition among sponsors intensifies as fintech demand grows and charters rise. Banks differentiate via maturity, compliance rigor, tech stacks, and product breadth (e.g., national vs. regional charters). Fintechs benefit from choice—better pricing, innovation support, and alignment—but sponsors grow selective, favoring partners with strong AML and risk profiles. This rivalry benefits the ecosystem by elevating standards and options.

Market map visualizing sponsor banks, BaaS platforms, and fintechs in the competitive landscape.

Why Partnerships Are the Future for Fintech (scale, credibility, compliance)

Partnerships deliver scale without full regulatory burden, credibility via FDIC-insured products, and shared compliance expertise. They enable faster launches, diversified revenue, and access to underserved markets. Even chartered fintechs partner for specialized needs. In a maturing industry, symbiotic relationships—where banks handle risk and fintechs drive innovation—outperform isolation, fostering sustainable growth.

BaaS Maturity: From Growth-at-All-Costs to Sustainable Models

Early BaaS emphasized rapid expansion, but failures highlighted risks. Maturity brings focus on quality partnerships, robust controls, and long-term alignment. Sponsors now prioritize sustainable fintechs with strong compliance, shifting from volume to value. This evolution supports healthier ecosystems, with direct contracts and tech investments replacing intermediaries.

Fintechs and Sponsor Banks: Symbiotic or Shifting Power Dynamics?

Historically symbiotic—fintechs innovate, banks provide rails—the dynamic is shifting toward balance. Sponsors gain leverage via stricter demands and competition, while scaled fintechs negotiate better or charter partially. True symbiosis persists when aligned: banks own ultimate risk, fintechs bring reach. Power tilts toward mutual benefit in mature setups.

Third-Party Risk Management in Bank-Fintech Collaborations

Regulators mandate strong third-party oversight—risk assessments, ongoing monitoring, and controls. Sponsors implement layered frameworks (e.g., three-tier compliance) to manage fintech risks. Fintechs must invest in AML, KYC, and data sharing to maintain partnerships. Effective management turns potential vulnerabilities into strengths, ensuring stability.

The End of Middleware BaaS Era (move to vertically integrated or direct partnerships)

Middleware platforms face decline as sponsors prefer direct fintech contracts for deeper alignment, control, and revenue. Banks build modern stacks for embedded finance, bypassing intermediaries. The shift favors vertically integrated models—direct partnerships or chartered entities—prioritizing efficiency, compliance, and scalability over layered tech. This matures BaaS into sustainable, high-value collaborations.

Comments