|

| Why Is MU Stock Dropping After Micron Beat Earnings? | EBC Financial Group |

Micron Technology (MU) smashes Wall Street forecasts amid surging AI demand for HBM memory chips, but shares trade lower after hours despite a 30% dividend hike and historic performance.

By Semiconductor Market Analyst Desk – March 19, 2026 Updated with official Micron data and independent analysis

Micron Technology delivered fiscal Q2 2026 results that far exceeded analyst projections, marking one of the strongest quarters in the company’s history. Adjusted earnings per share hit $12.20—crushing the consensus estimate of $9.19 and soaring from $1.56 a year ago. Revenue reached $23.86 billion (rounded as $23.9 billion in reports), topping expectations of around $20 billion and surging 196% year-over-year.

|

| Micron Technology: HBM Sold Out For 2026, Wall Street Is Still Underpricing (NASDAQ:MU) | Seeking Alpha |

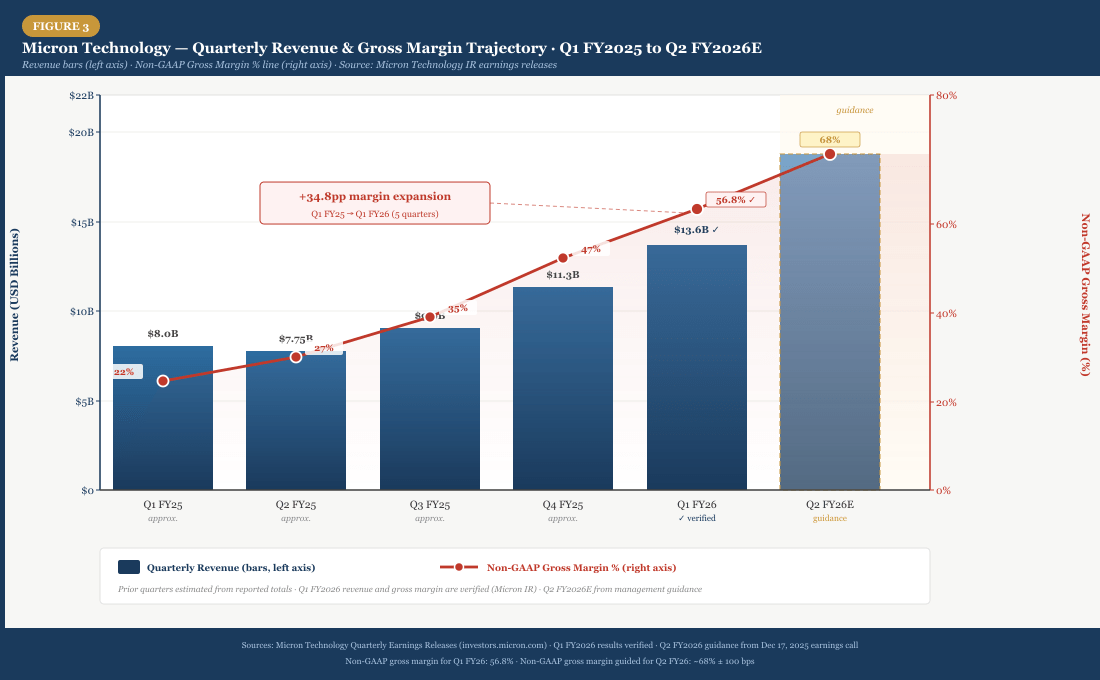

Figure: Micron’s quarterly revenue and non-GAAP gross margin trajectory from Q1 FY2025 to Q2 FY2026 guidance Source: Independent compilation of Micron IR data. The explosive growth reflects AI-driven pricing power and tight supply.

Original Analysis: This isn’t just another cyclical upswing. For over a decade, Micron and its peers operated in a commodity memory business tied to PCs and smartphones. Today, high-bandwidth memory (HBM) for AI accelerators has transformed the industry into a high-margin, structurally tight market. Data-center sales jumped 181%, while even non-data-center segments rose 219%, showing demand rippling across the entire supply chain.

|

| High-bandwidth memory (HBM) | Micron Technology Inc. |

Figure: Micron HBM3E memory stack integrated with GPU – the core of AI data-center acceleration High-bandwidth memory chips like these are sold out through 2026, driving Micron’s record 81% gross-margin guidance.

CEO Sanjay Mehrotra opened the earnings call with confidence: “Micron delivered an exceptional fiscal Q2… Quarterly revenue nearly tripled versus one year ago. Our fiscal Q3 single-quarter revenue guidance exceeds the full-year revenue for every year in our company’s history through fiscal 2024.”

|

| Sanjay Mehrotra | Micron Technology Inc. |

Figure: Sanjay Mehrotra, Chairman, President and CEO of Micron Technology Under his leadership, Micron has positioned itself as a key enabler of the AI infrastructure boom.

Strong Q3 Guidance Signals Continued Acceleration

Micron raised the bar again for the current quarter:

- Revenue: ~$33.5 billion (±$0.75 billion)

- Gross margin: ~81%

- Adjusted EPS: ~$19.15

These figures eclipse prior full-year records and reflect sustained pricing strength plus accelerating HBM shipments. No major new memory capacity is expected until mid-2027, creating a multi-year tailwind that analysts say could overwhelm traditional cyclicality.

While consumer electronics demand remains strong, the real game-changer is AI infrastructure. Memory makers are no longer victims of oversupply cycles; they are now capacity-constrained beneficiaries of a secular shift. Micron’s decision to raise fiscal 2026 capital expenditures above $25 billion (including new fabs) shows management is investing aggressively to capture this demand—yet supply will still lag, supporting elevated margins through at least 2027.

Stock Reaction: Extraordinary Results, Temporary Dip

Despite the blowout numbers and a 30% dividend increase, Micron shares traded roughly 1% lower in after-hours trading immediately following the release (later reports showed some recovery intraday volatility).

| How to build an AI Datacentre — Part 1 (Cooling and Power) | by elongated_musk | Medium |

Figure: Inside a modern AI data center – where Micron’s HBM and DRAM power thousands of GPU servers Demand from hyperscalers has created the most severe memory shortage in a generation.

Markets sometimes digest “sell the news” after parabolic runs. Micron stock has already delivered massive gains in recent months on AI hype. Profit-taking is normal, especially when guidance—while stellar—meets elevated expectations. Long-term, the combination of sold-out HBM through 2026, 81% margins, and record free cash flow ($6.9 billion in Q2) paints a compelling picture for patient investors.

Micron has entered a new era. The AI data-center boom has turned memory from a cyclical commodity into a strategic, high-margin growth engine. While the immediate stock reaction reflects profit-taking, the fundamentals—record results, blockbuster guidance, and persistent supply shortages—position Micron for sustained outperformance through 2027 and beyond.

Comments