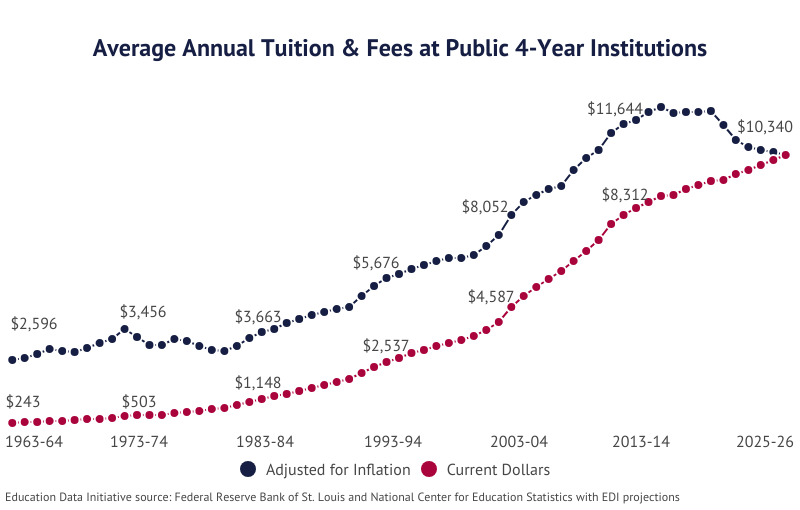

As of mid-April 2026, the federal student loan landscape has undergone its most significant transformation in decades. Following the passage of the One Big Beautiful Bill Act (OBBBA), the Trump administration has effectively "reset" the borrowing and repayment system, with most changes slated to go live on July 1, 2026.

Whether you are a current borrower, a parent, or a prospective graduate student, here is the real-time breakdown of the 2026 overhaul.

The "One Big Beautiful Bill" Act: Core Changes

The administration’s policy focuses on two pillars: simplification and market-driven borrowing caps. The goal is to curb tuition inflation by limiting how much the federal government will lend.

1. New Borrowing Caps (Effective July 1, 2026)

The days of unlimited federal borrowing for graduate school (Grad PLUS) are ending. New annual and lifetime limits are being implemented to force schools to lower costs.

| Student Category | Annual Loan Limit | Lifetime (Aggregate) Limit |

|---|---|---|

| Graduate Students | $20,500 | $100,000 |

| Professional (MD, JD, etc.) | $50,000 | $200,000 |

| Parent PLUS Borrowers | $20,000 per student | $65,000 per student |

Note: The "Nursing Gap": Currently, nursing and public health programs are categorized as "Graduate" rather than "Professional," effectively halving the amount these students can borrow compared to law or medical students.

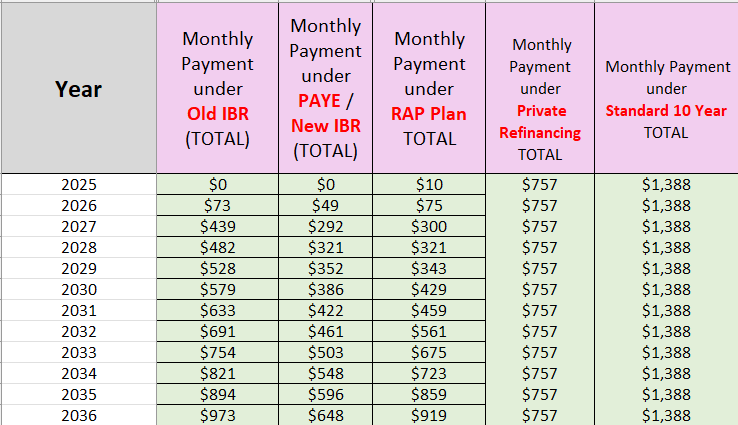

The "RAP" Era: A Two-Plan System

Starting July 1, 2026, the complex web of repayment plans (SAVE, PAYE, ICR, etc.) is being replaced by just two choices for new borrowers:

Plan A: The New Standard Plan A fixed monthly payment model where the duration is dictated by your total debt:

- <$25k: 10-year term.

- $25k – $50k: 15-year term.

- $50k – $100k: 20-year term.

- $100k+: 25-year term.

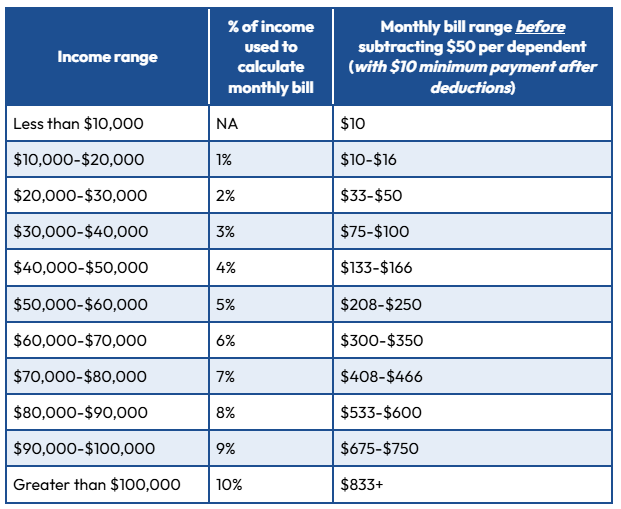

Plan B: Repayment Assistance Plan (RAP) This is the new primary Income-Driven Repayment (IDR) plan.

Payments: Calculated at 1% to 10% of your adjusted gross income (AGI). The Floor: If your income is below $10,000/year, your payment is a flat $10/month. Interest Benefit: RAP eliminates negative amortization. If your payment doesn't cover the interest, the government pays the rest. They will also pay up to $50 of your principal monthly for on-time payments. Forgiveness: Any remaining balance is forgiven after 30 years of repayment.

The "Exception" Clauses: Who is Grandfathered?

The 2026 rules include a critical "Legacy Provision" to prevent immediate shock to current students.

The 2029 Rule: Students who received a Grad PLUS loan before July 1, 2026, and remain in the same program can continue borrowing under the old "cost of attendance" rules until June 30, 2029.

The 2028 Sunset: If you are currently on a SAVE, PAYE, or ICR plan, you can stay on it for now. However, you must transition to either IBR (Income-Based Repayment) or RAP by July 1, 2028.

Parent PLUS Exception: Parent PLUS loans are not eligible for the new RAP plan. To access income-driven repayment, parents must consolidate their loans before the July 1, 2026, deadline.

Forgiveness & Relief Updates

PSLF (Public Service Loan Forgiveness): Remains active and unchanged by the OBBBA. Forgiveness after 10 years for public servants is still the law of the land.

Bankruptcy & Defaults: In a surprise policy shift, the administration has announced it will not garnish wages for borrowers in default, though Social Security garnishment for older borrowers remains a point of legal contention.

Economic Hardship: Loans taken out after July 1, 2027, will no longer be eligible for "Unemployment Deferment." Borrowers will be encouraged to use the $10/month RAP payment instead.

If you are planning on graduate school or need to consolidate, act before July 1, 2026. This is the hard cutoff date where "Legacy" status is determined. After that, you are officially in the "One Big Beautiful" system.

Are you currently enrolled in a program, or are you looking at starting a new degree under these 2026 limits?

Comments