Palantir Technologies (NYSE: PLTR) powers AI-driven decision-making for governments and enterprises via its Artificial Intelligence Platform (AIP), Foundry, and Gotham.

What is Palantir Technologies

Palantir Technologies builds software platforms that turn complex data into actionable intelligence. Founded in 2003, it went public in 2020. Its core products—AIP (launched 2023), Foundry, and Gotham—use ontology-based AI to integrate siloed data, run agentic workflows, and enable real-time decisions. Revenue splits between government (stable, high-margin contracts) and commercial (explosive U.S. growth). As of April 2026, market cap sits around $312B (intraday), with TTM revenue of $4.48B, 36.31% profit margins, and 70%+ quarterly YoY growth in recent periods. Palantir operates a high-margin SaaS-like model with intensive “Bootcamp” deployments that convert pilots into multi-year contracts.

What is the current PLTR stock price and market performance?

(as of ~10:27 AM EDT, 9 April 2026 market open):

- Price: $130.40 USD

- Change: –$10.35 (–7.36%)

- Previous Close: $140.76

- Day’s Range: $129.80 – $139.40

- 52-Week Range: $84.14 – $207.52

- Volume: 28.8M (vs. 3-mo avg. 49.6M)

- Market Cap: ~$312B

PLTR has been volatile in 2026, recently down amid broader AI rotation and competition concerns (e.g., Anthropic). However, it remains up significantly YTD and over 1-year on strong commercial momentum. Beta of 1.67 confirms higher volatility than the market.

Palantir earnings report – what did the latest results show?

Q4 2025 was record-setting: ~70% YoY revenue growth, U.S. commercial revenue +137%, and total contract value ~$4.3B. Full-year 2026 guidance calls for ~61% revenue growth to ~$7.2B. Adjusted operating income margins remain strong. Next earnings: estimated May 4, 2026. Analysts expect Q1 2026 revenue ~$1.54B and EPS $0.28. Commercial acceleration (especially U.S.) is the standout driver.

PLTR stock forecast, target price, and long-term outlook

- Analyst Consensus 1-Year Target: $185.25 (implying ~42% upside from current levels)

- 2026 EPS Estimate: $1.32 (76% growth)

- 2027 EPS Estimate: $1.86 (41% growth)

- 2026 Revenue Estimate: $7.26B

- 2027 Revenue Estimate: $10.39B

Long-term: Next 5-year growth remains robust due to AIP’s “ontology + agentic AI” edge. CEO Alex Karp calls Palantir the “n of 1” in enterprise AI operating systems. Wall Street sees sustained 40%+ commercial growth if Bootcamps continue converting at current rates.

Is Palantir a good investment? Buy or sell? Risks and rewards

Rewards:

- Explosive U.S. commercial growth (115%+ guided for 2026)

- 36%+ profit margins with operating leverage

- Sticky government contracts + AI moat via ontology layer

- Proven execution in 2025–2026

Risks:

- Sky-high valuation (trailing P/E ~207, forward ~109, Price/Sales ~81) leaves little margin for error

- Competition from hyperscalers and pure-play AI tools

- Recent 7%+ single-day drops highlight volatility

- Macro slowdown could delay enterprise AI budgets

Bottom line (balanced view): Strong buy for growth-oriented investors with 3–5+ year horizon who tolerate volatility. Not ideal for value investors or short-term traders. Many analysts rate it Buy/Outperform.

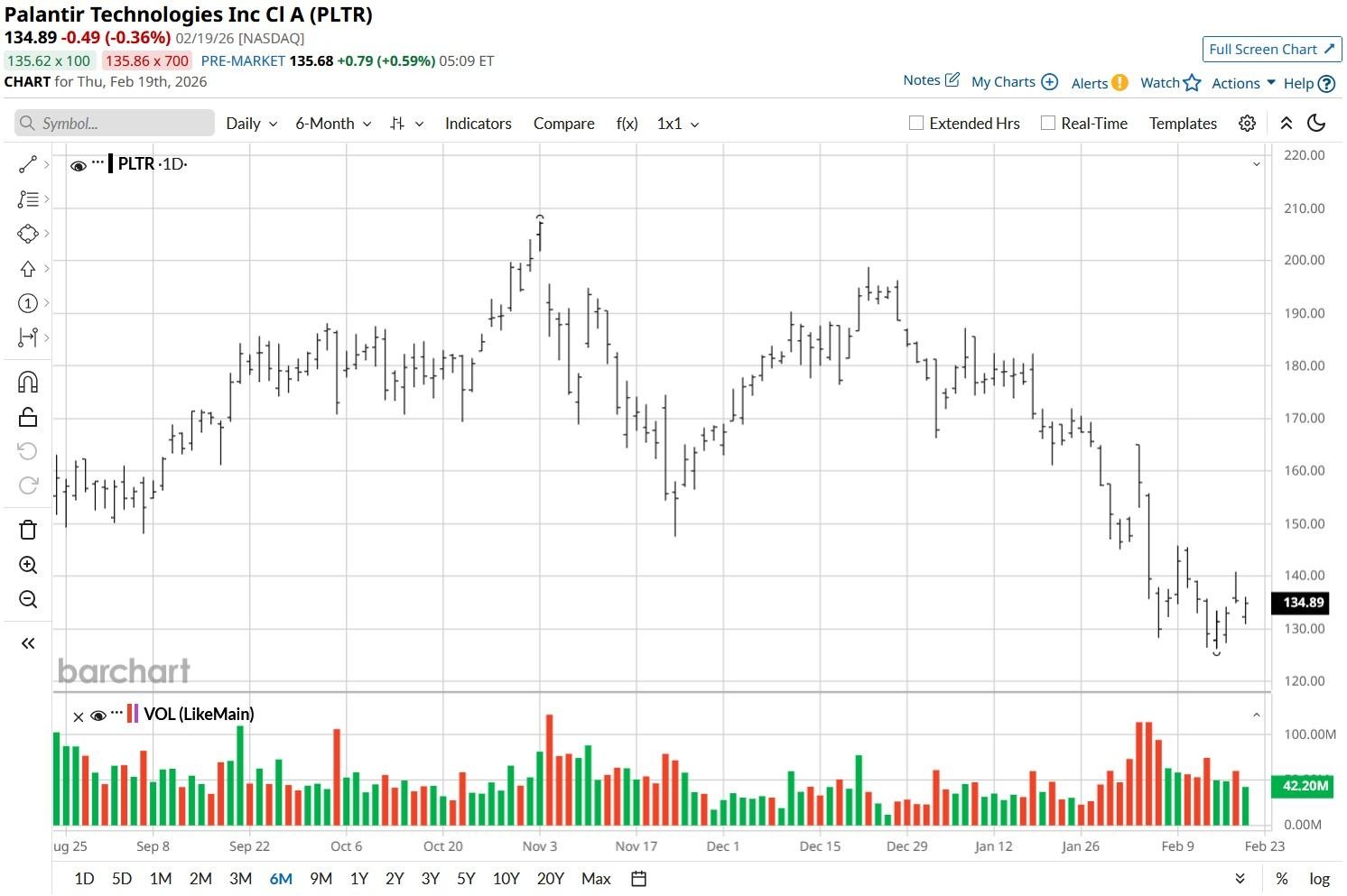

PLTR stock technical analysis – support and resistance levels

Recent charts show a head-and-shoulders pattern with neckline breakdown. Key levels (April 2026):

- Immediate Support: $129–$130 (today’s low) → next major at ~$116–$128

- Resistance: $140–$145 (recent breakdown area) → then $156–$162

- Short-term projection (next 25 days): $140–$160 range if momentum stabilizes

RSI and MACD show oversold conditions post-drop, but confirmation needed above $140 for bullish reversal. High volatility (ATR ~7) expected.

Palantir business model explained

Palantir sells enterprise AI operating systems, not generic LLMs. Revenue model: high-margin software licenses + services via Bootcamps (5-day intensive workshops where clients build live AI use cases on their data). Two segments:

- Government (stable, long-term contracts with DoD, intelligence, NHS)

- Commercial (Fortune 500 in manufacturing, energy, finance – fastest growing)

The “ontology” layer maps real-world data/assets/workflows, turning AIP into agentic systems that execute decisions inside existing processes. Scalable SaaS economics with 31–40% operating margins.

Palantir competitors in 2026

Direct/indirect: ServiceNow (NOW), Snowflake (SNOW), Datadog (DDOG), CrowdStrike (CRWD), Broadcom (AVGO) for AI/enterprise platforms. Broader: Microsoft (Azure + Copilot), Amazon (AWS), Google. Palantir differentiates with defense-grade security, ontology depth, and Bootcamp conversion rates. It often outperforms peers on revenue growth (56%+ LTM) but trades at premium multiples.

PLTR institutional investors and ownership

Institutions own 61.47% of shares (3,709 institutions). Top holders (as of Dec 31, 2025 filings):

- Vanguard Group – 9.88%

- BlackRock – 8.87%

- State Street – 4.70%

- Geode Capital – 2.49% …and others (JPM, Morgan Stanley, Norges Bank). Insider ownership: 3.59%. Heavy institutional backing signals long-term confidence.

Palantir strategic partnerships (latest 2026 updates)

- Stellantis: 5-year renewal/expansion (March 2026) – full AIP + Foundry rollout

- Nvidia: Sovereign AI operating system architecture

- Accenture: Global strategic alliance for enterprise AI transformation

- GE Aerospace: AI for military aircraft readiness & production

- LG CNS: Expanded AI initiatives in Asia

These partnerships accelerate commercial adoption and validate AIP’s industrial use cases.

Palantir stock volatility, review, and risks/rewards summary

Beta 1.67 + recent 7%+ swings = high volatility. 2026 has seen sharp pullbacks amid AI rotation, yet fundamentals (70% growth quarters) remain intact. Review: Best-in-class AI execution but valuation demands perfection. Rewards outweigh risks for believers in enterprise AI operating systems.

How to buy PLTR stock

- Open a brokerage account (e.g., Fidelity, Charles Schwab, Robinhood, Zerodha in India).

- Search ticker “PLTR”.

- Place market/limit order (available on NYSE).

- Consider dollar-cost averaging due to volatility.

- Hold in taxable or tax-advantaged accounts. Consult a financial advisor – this is not personalized advice.

Palantir stock potential and future prospects

AIP is positioned as the “enterprise AI operating system.” If Palantir converts Bootcamps at scale and maintains 40%+ growth into 2027–2028, the stock has multibagger potential over 5 years. Government tailwinds (defense AI) + commercial inflection make 2026–2027 pivotal. Watch May 2026 earnings for commercial acceleration confirmation.

Palantir is a high-growth, high-valuation AI leader with real products and customers. Current dip may represent a buying opportunity for long-term investors, but always do your own research. Stock investing involves risk of loss. Data current as of April 9, 2026 market open – prices move fast.

Comments