Understanding the basic rules of monthly retirement payments

Navigating the modern landscape of long-term financial planning requires a deep understanding of how the Social Security administration manages the safety net millions of Americans rely on daily. As we look at the landscape in 2026, staying ahead of major Social Security news and policy modifications is no longer optional; it is a foundational necessity for anyone aiming to maximize their future wealth. For generations, these government-backed retirement benefits have served as the cornerstone of post-work independence, ensuring that long careers translate into predictable, reliable lifetime cash flow. When discussing Social Security for seniors, the focus typically lands on replacing a portion of your career income, but the scope of the program expands far beyond a simple monthly stipend. Successfully managing your future Social Security income requires viewing it not as a passive government handout, but as an earned asset that demands active strategic planning, routine check-ins, and precise timing. By treating these benefits as an adjustable financial tool rather than a fixed guarantee, workers can better insulate their households from economic volatility and establish a truly resilient retirement base.

Navigating the modern landscape of long-term financial planning requires a deep understanding of how the Social Security administration manages the safety net millions of Americans rely on daily. As we look at the landscape in 2026, staying ahead of major Social Security news and policy modifications is no longer optional; it is a foundational necessity for anyone aiming to maximize their future wealth. For generations, these government-backed retirement benefits have served as the cornerstone of post-work independence, ensuring that long careers translate into predictable, reliable lifetime cash flow. When discussing Social Security for seniors, the focus typically lands on replacing a portion of your career income, but the scope of the program expands far beyond a simple monthly stipend. Successfully managing your future Social Security income requires viewing it not as a passive government handout, but as an earned asset that demands active strategic planning, routine check-ins, and precise timing. By treating these benefits as an adjustable financial tool rather than a fixed guarantee, workers can better insulate their households from economic volatility and establish a truly resilient retirement base.

To unlock the true potential of your foundational Social Security benefits, you must first master the core principles governing Social Security eligibility and how your baseline checks are calculated. The system looks closely at your highest 35 years of indexed earnings, which means that any gaps in your employment history can dilute the size of your ultimate Social Security checks. Many working professionals mistakenly assume that the system operates on an autopilot setting, but true optimization requires you to actively audit your yearly earnings statements via your online government account. Our collective analysis shows that even minor reporting errors by employers can permanently drag down your monthly checks if they are left uncorrected before you formally file. Furthermore, understanding the threshold for maximum Social Security benefits involves recognizing the cap on taxable earnings, which has climbed significantly this year to meet shifting macroeconomic realities. Knowing exactly how these baselines are structured allows you to deploy targeted Social Security tips, such as boosting your income during your peak earning years to push out lower-earning years from your historical record.

Navigating the hidden steps for choosing your claim age

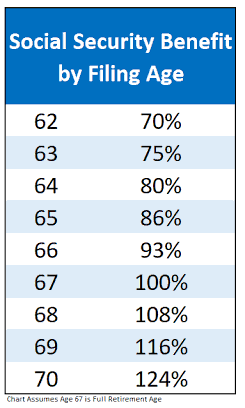

Social Security Benefit Percentages by Filing Age

Choosing the exact moment to transition from worker to beneficiary represents one of the most critical financial milestones of your life, heavily dictated by the shifting Social Security retirement age guidelines. For anyone born in 1960 or later, reaching full retirement age now requires waiting until age 67 to collect 100% of your earned benefit, a structural reality that catches many future retirees off guard. Filing early at age 62 triggers a permanent reduction in your monthly income, whereas delaying your application up until age 70 unlocks compounding delayed retirement credits that permanently elevate your base pay. From an independent consulting perspective, the decision shouldn't merely rest on a generic break-even calculation; it must account for your personal health history, tax bracket changes, and whether you plan to continue working. Working while collecting before your full retirement age subjects your Social Security payments to strict earnings limits, where exceeding the annual limit results in temporary benefit withholding. This intricate interplay between age, active employment, and benefit size highlights why generic advice fails and why customized, age-specific roadmaps are indispensable for preserving long-term wealth.

| Social Security Benefit Percentages by Filing Age |

What happens when health issues change your working life

Life rarely follows a linear path, and when severe health challenges disrupt your ability to earn a living, the discussion must pivot toward vital disability benefits. Securing Social Security for disability involves navigating a highly rigorous evaluation process where the government assesses whether your medical condition meets their strict definition of a total, long-term impairment. This specialized branch of Social Security assistance acts as an essential financial lifeline, providing stable monthly support to individuals who can no longer engage in substantial gainful activity due to physical or cognitive limitations. Industry analysis confirms that filing a claim for these specialized funds requires meticulous documentation, extensive medical records, and often a healthy dose of patience given the historically high rate of initial application denials. Navigating this bureaucratic maze requires a proactive approach, ensuring that your medical providers explicitly document how your limitations prevent routine workplace tasks. By understanding how these specific disability safety nets operate alongside traditional retirement structures, vulnerable workers can protect their families from sudden, catastrophic income drops during their most challenging seasons.

Life rarely follows a linear path, and when severe health challenges disrupt your ability to earn a living, the discussion must pivot toward vital disability benefits. Securing Social Security for disability involves navigating a highly rigorous evaluation process where the government assesses whether your medical condition meets their strict definition of a total, long-term impairment. This specialized branch of Social Security assistance acts as an essential financial lifeline, providing stable monthly support to individuals who can no longer engage in substantial gainful activity due to physical or cognitive limitations. Industry analysis confirms that filing a claim for these specialized funds requires meticulous documentation, extensive medical records, and often a healthy dose of patience given the historically high rate of initial application denials. Navigating this bureaucratic maze requires a proactive approach, ensuring that your medical providers explicitly document how your limitations prevent routine workplace tasks. By understanding how these specific disability safety nets operate alongside traditional retirement structures, vulnerable workers can protect their families from sudden, catastrophic income drops during their most challenging seasons.

Providing continuous financial security for the family left behind

A frequently overlooked component of this federal infrastructure is the robust layer of protection built specifically as Social Security for families facing unexpected loss. Shifting our focus to survivor benefits reveals a critical shield for dependents, providing essential ongoing financial continuity when a household's primary breadwinner passes away. Dedicated provisions like Social Security survivor benefits ensure that minor children, dependent parents, and grieving partners do not face immediate financial ruin alongside their emotional grief. Specifically, analyzing the nuances of Social Security for widows highlights complex rules regarding age, marriage duration, and the strategic choice between claiming a personal retirement benefit or a deceased partner's higher benefit rate. Maximizing these family-focused protections requires understanding how household benefit caps limit the total monthly sum distributed to a single family unit. Embracing these protections as a core element of your broader life insurance and estate planning conversations ensures that your loved ones remain fully insulated from poverty, preserving your financial legacy across multiple generations.

A frequently overlooked component of this federal infrastructure is the robust layer of protection built specifically as Social Security for families facing unexpected loss. Shifting our focus to survivor benefits reveals a critical shield for dependents, providing essential ongoing financial continuity when a household's primary breadwinner passes away. Dedicated provisions like Social Security survivor benefits ensure that minor children, dependent parents, and grieving partners do not face immediate financial ruin alongside their emotional grief. Specifically, analyzing the nuances of Social Security for widows highlights complex rules regarding age, marriage duration, and the strategic choice between claiming a personal retirement benefit or a deceased partner's higher benefit rate. Maximizing these family-focused protections requires understanding how household benefit caps limit the total monthly sum distributed to a single family unit. Embracing these protections as a core element of your broader life insurance and estate planning conversations ensures that your loved ones remain fully insulated from poverty, preserving your financial legacy across multiple generations.

How recent changes protect your cash from rising prices

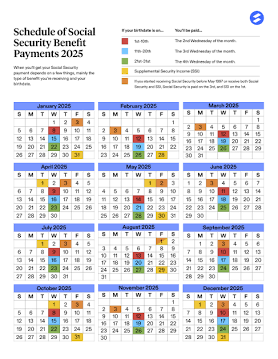

Social Security Monthly Payment Distribution Schedule

Maintaining your purchasing power throughout a decades-long retirement requires a dynamic mechanism to counteract the eroding effects of inflation, which is where the annual Social Security cost of living adjustment plays a defining role. The latest Social Security updates for 2026 bring a welcome 2.8% Social Security increase, a direct reflection of shifting consumer price patterns intended to keep your household budget balanced against rising everyday expenses. This automatic adjustment mechanism prevents fixed-income seniors from falling behind as food, healthcare, and utilities inevitably grow more expensive over time. From an analytical perspective, while a 2.8% bump provides a necessary cushion, savvy retirees must recognize that their personal inflation rate, particularly regarding medical costs, often outpaces the broader government index. Consequently, relying solely on this annual boost to maintain your standard of living can be risky, underscoring the absolute necessity of pairing your government checks with personal investments. Tracking these regular adjustment cycles allows you to adjust your broader portfolio withdrawal rates systematically, keeping your comprehensive financial plan perfectly aligned with current economic realities.

| Social Security Monthly Payment Distribution Schedule |

Simple steps to securely lock in your monthly checks

When you are finally ready to transition from planning to action, mastering how to apply for Social Security efficiently becomes your primary operational objective. The modern application process has been heavily digitized, allowing you to launch your claim through the secure online portal without ever stepping foot inside physical Social Security offices. During this final phase, establishing a seamless Social Security direct deposit link is paramount to ensure your funds bypass the mail entirely and land safely in your bank account on your assigned Social Security payment dates. Reviewing the official Social Security payment schedule reveals that your specific distribution day is determined entirely by your birth date, creating a highly predictable cash flow cycle for your monthly budgeting. For those facing complex scenarios or unique household circumstances, diving into comprehensive Social Security resources and official Social Security FAQs can resolve lingering uncertainties before you submit your final forms. Taking charge of this final onboarding process with precision ensures a stress-free launch to your retirement, cementing decades of hard work into a stable, golden future.

When you are finally ready to transition from planning to action, mastering how to apply for Social Security efficiently becomes your primary operational objective. The modern application process has been heavily digitized, allowing you to launch your claim through the secure online portal without ever stepping foot inside physical Social Security offices. During this final phase, establishing a seamless Social Security direct deposit link is paramount to ensure your funds bypass the mail entirely and land safely in your bank account on your assigned Social Security payment dates. Reviewing the official Social Security payment schedule reveals that your specific distribution day is determined entirely by your birth date, creating a highly predictable cash flow cycle for your monthly budgeting. For those facing complex scenarios or unique household circumstances, diving into comprehensive Social Security resources and official Social Security FAQs can resolve lingering uncertainties before you submit your final forms. Taking charge of this final onboarding process with precision ensures a stress-free launch to your retirement, cementing decades of hard work into a stable, golden future.

Comments